Medicare Advantage vs. Medicare Supplement: A Plain-English Comparison

Medicare Advantage (Part C) bundles your coverage into one plan, often with extra benefits and a low or $0 premium, but with networks and rules. Medicare Supplement (Medigap) pairs with Original Medicare to cover many of your out-of-pocket costs, with more freedom to see any doctor who takes Medicare, usually at a higher monthly premium. Neither is "better" — they're two different ways to handle the gaps in Original Medicare.

First, the gap both are solving

Original Medicare (Parts A and B) covers a lot, but not everything — it has deductibles, coinsurance, and no out-of-pocket maximum, and it doesn't include prescription drug coverage on its own. Medicare Advantage and Medicare Supplement are two different strategies for filling those gaps.

Medicare Advantage (Part C)

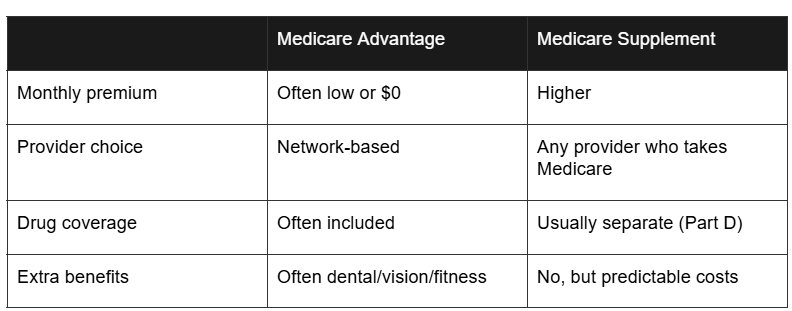

An Advantage plan, offered by private carriers, replaces the way you receive your Medicare benefits and usually bundles everything together — often including Part D drug coverage and extras like dental, vision, or fitness benefits. Premiums are frequently low or $0, but you typically use a network of providers and may need referrals or prior authorizations. Your costs come as copays and coinsurance as you use care, up to an annual out-of-pocket maximum.

Medicare Supplement (Medigap)

A Supplement plan works alongside Original Medicare and helps pay the out-of-pocket costs Medicare leaves behind, like coinsurance and deductibles. You can generally see any provider in the country who accepts Medicare — no networks — which is great for travelers and people who want maximum flexibility. The trade-off is a higher monthly premium, and you'll usually add a separate Part D drug plan.

The quick comparison

How to think about which fits

Many people who want the lowest monthly cost and don't mind a network lean toward Advantage; many who want maximum freedom and predictable costs — especially frequent travelers — lean toward Supplement. But the right answer depends on your doctors, your medications, your budget, and your health. This is exactly the kind of decision where an independent broker who knows your situation makes a real difference.

Frequently asked questions

Can I switch between them later?

Sometimes, but rules and timing matter — and switching to a Supplement later may involve health questions. It's worth getting it right the first time.

Which is cheaper?

Advantage usually has a lower monthly premium; Supplement often means fewer surprise costs when you use care. "Cheaper" depends on how much care you use.

Do I still need Part D?

With a Supplement, usually yes (separately). With many Advantage plans, drug coverage is built in.

How do I choose?

Start with your doctors and prescriptions, then weigh budget and flexibility — or let us compare your options for you.

Let's make Medicare make sense

Medicare doesn't have to be overwhelming. Learn more about Medicare or talk to a licensed agent at 385-317-4119 — we'll walk you through every option with zero pressure.

This article is for general educational purposes only and is not insurance or medical advice. We do not offer every plan available in your area. Any information we provide is limited to the plans we do offer in your area — we currently represent ___ organizations which offer ___ products in your area. Please contact Medicare.gov, 1-800-MEDICARE, or your local State Health Insurance Assistance Program (SHIP) to get information on all of your options. Not connected with or endorsed by the United States government or the federal Medicare program.